Landscaping business valuation is the process of estimating what a landscaping company is worth based on earnings, cash flow, growth potential, assets, and risk, so owners, buyers, and investors can make informed decisions about selling, buying, or scaling. The global landscaping and gardening services market is valued at $123.48 billion in 2024 and projected to reach $201.9 billion by 2034.

Today’s buyers look past surface size to measure durable earnings, risk, and how easily a firm can transfer to new ownership.

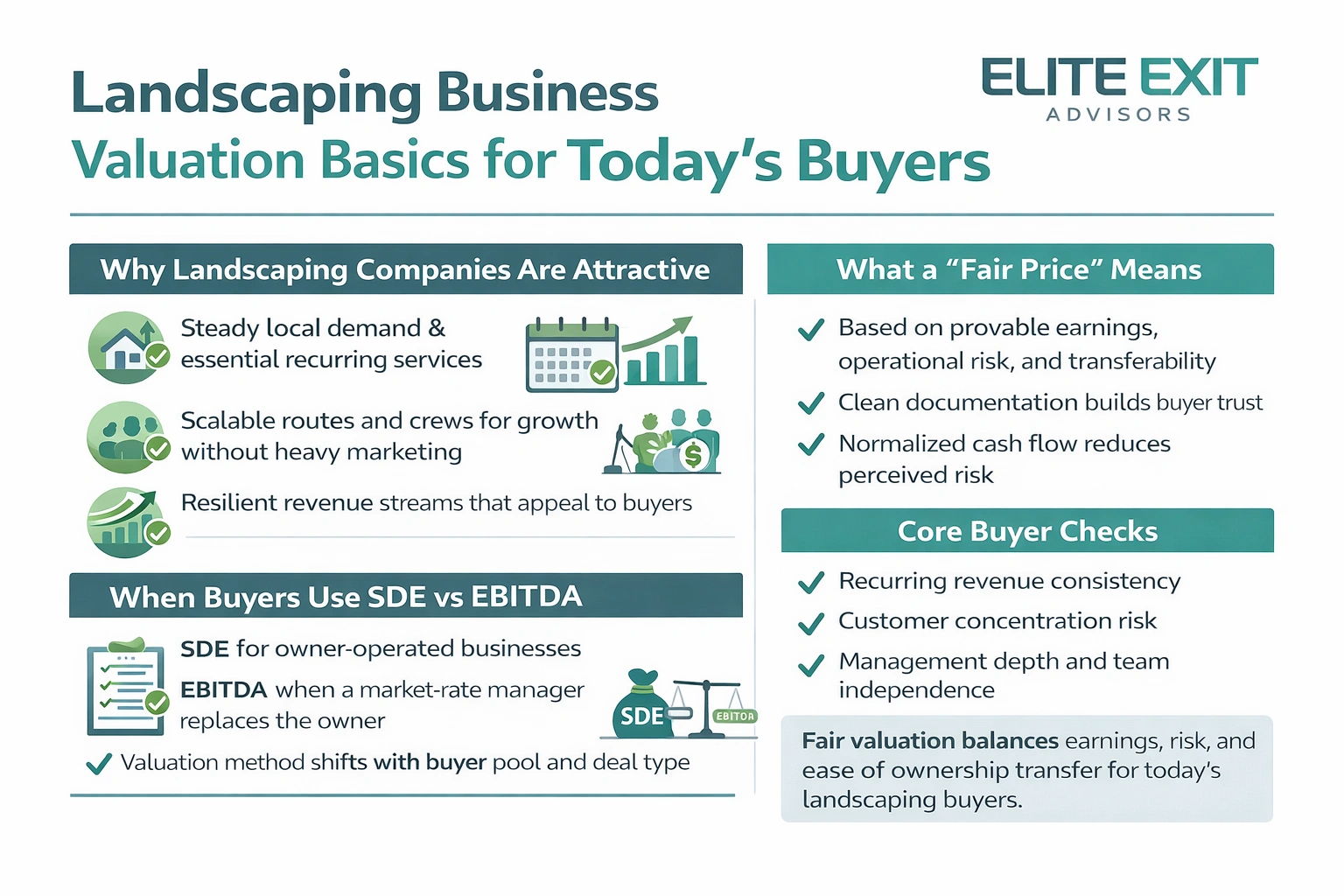

Essential recurring services and steady local demand make many companies resilient. Routes and crews scale logically, letting a buyer grow revenue as they add accounts or crews without heavy marketing spend.

Buyers define fair price by provable earnings, operational risk, and transferability. Clean documentation of cash flow and normalized earnings builds trust and reduces perceived risk.

A buyer prefers SDE for owner-operator deals where the owner’s pay skews results. EBITDA is used when a market-rate manager replaces the owner and institutional buyers enter the pool.

Buyers most often rely on earnings multiples because those figures tie offers to real cash flow and risk. The multiple-of-earnings method converts normalized profit into a price range that buyers can justify to lenders and partners.

The method compares adjusted owner profit to market norms. Buyers prefer it over simple rules because it accounts for expenses, seasonality, and one-time items.

Industry ranges commonly observed are 2–4× SDE for owner-operated firms and 5–7× EBITDA for management-run companies. Exact multiples depend on risk profile, contract mix, and deal terms.

"Comparable sales" means recent deals with similar size, geography, service mix, customer concentration, and margins. Buyers treat these comps as the market signal that beats informal formulas.

Seller’s Discretionary Earnings (SDE) captures the total economic return a working owner can extract from a firm in a typical year. It converts reported numbers into the cash a new owner would receive before owner-specific items are removed.

Start with net profit, then add back the owner’s salary and any owner draws. Include owner benefits and personal expenses run through company accounts.

Sophisticated buyers want consistent statements, reconciled accounts, and clear categories for owner draws and personal items.

Documentation matters: add-backs must link to invoices, payroll records, or tax returns. Unsupported adjustments get discounted.

Valuation impact: because price follows an earnings multiple, under-reporting $1 of cash can reduce value roughly $2–$3 or more, depending on the multiple and buyer expectations.

Buyers use EBITDA to see how a company performs without financing or tax differences clouding the picture. EBITDA adds back interest, taxes, depreciation, and amortization so a buyer can compare operational profitability across firms in the same market.

EBITDA removes financing choices and tax treatments from earnings. That gives buyers a cleaner view of recurring operating profit.

This adjustment also replaces owner-specific pay with a market-rate officer salary when applicable.

When a company runs with management depth and systems, buyers see lower transfer risk. That often raises offer multiples.

Higher revenue and scalable processes attract lenders and strategic buyers who underwrite on EBITDA metrics.

As revenue grows into the multi-million-dollar range, buyers change. More sophisticated buyers and lenders evaluate deals on EBITDA, not SDE.

Higher multiples are possible but not guaranteed; buyers still examine margins, contracts, labor stability, and working capital needs.

Practical tip: Transitioning from owner-led to team-led operations usually moves discussions toward EBITDA logic.

Top-line sales can look impressive, but they often hide what a buyer really pays for: repeatable cash flow. Using a straight percentage of revenue or a 1–1.5× sales rule ignores profit, overhead, seasonality, and capital needs.

Revenue shows size, not economic value. Two firms with identical sales can have very different margins, labor stability, and equipment costs.

Buyers will not pay a high price for weak or negative profit. Lenders underwrite to cash flow, not to how big the top line reads.

Consider a $2M revenue company that runs thin margins after payroll and fuel. It can appear large but lose money after reinvestment.

A rational buyer discounts that risk or walks away. Paying for sales without sustainable earnings invites heavy retrades and failed deals.

Transferability, clean cash flow, and predictable demand are the clearest drivers of a higher multiple. Buyers prize firms that can run without daily owner input and that show steady earnings and low surprise risk.

When an owner steps back and a trained management team runs operations, transfer risk falls. That shift often raises the multiple because new owners can step in without disruption.

Buyers flag accounts that represent a large share of revenue. A few big customers increase renegotiation and churn risk. Diversified customer mix keeps offers higher and more competitive.

Slow payers force extra cash on hand for payroll and vendors. Receivables over 30 days lower buyer appetite and can reduce financing options. Clean, fast collections support stronger deal terms.

Smaller sales often face limited lender interest in the U.S., especially below about $350,000. That narrows buyer pools and can pressure price or require seller financing.

Consistent positive reviews and clear testimonials reduce perceived market risk. Public trust signals speed buyer confidence and help preserve multiples.

Reliable online leads and repeatable digital channels cut revenue volatility. Buyers pay more when growth sources are visible and not owner-dependent.

Dependable crews and documented hiring and training reduce operational interruption. A robust people system protects service quality and supports higher offers.

Repeat service routes and long-term contracts matter because they smooth seasonality and make cash flow predictable. Buyers value steady service revenue over sporadic installation work. Predictable routes allow crews to plan and reduce per-job expenses.

Contracts raise route density and lower marketing spend. They support higher offers because revenue is visible and less volatile. One-off projects boost top line but add selling and scheduling risk.

Commercial accounts tend to pay on schedule and renew annually. That reduces pricing pressure and churn. A heavy residential mix may show higher peaks and deeper troughs, which buyers discount.

Buyers treat undocumented hiring as a major red flag. Penalties can range from $375 to $3,000 per employee, and severe legal consequences are possible. Noncompliance can stop a deal or force a heavy discount.

Buyers inspect age, maintenance logs, and replacement cycles. If stated depreciation understates real wear, buyers increase assumed expenses post-close. Clean records reduce perceived risk.

Why it matters: predictable services, legal compliance, and reliable equipment lower buyer risk and protect post-close operations.

Matching the right buyer type to your goals changes price, timing, and post-close expectations. Decide first whether you want maximum cash at close, speed, confidentiality, to keep staff, or to stay on in operations.

Individual buyers often suit mid-six to low-seven figure sales. They typically step into day-to-day leadership and pay for a turnkey operation.

Why it helps: smoother transition, fewer structural demands, and simpler financing for the buyer.

Competitors may discount goodwill, redundant staff, or nonconforming assets. Strategic buyers pay for synergies and market share, so price can differ.

Expect competitors to focus on cost savings; strategics value integration and growth potential.

Private equity offers partial cash now and retained equity for a later exit. Deals often include a negotiated role and performance milestones.

This route can raise scale quickly but brings increased reporting and governance demands.

Employee buyouts preserve culture and continuity but need solid financing and clear leadership plans. They appeal when keeping crews and clients is a priority.

Business brokers and online marketplaces widen exposure and generate multiple buyers. Keep control with strict confidentiality, strong buyer screening, and clear process rules.

A typical sale follows a clear workflow from preparation to close, and knowing each step reduces surprises. The end-to-end process usually runs: prepare financials, set price, market the company, screen buyers, receive LOIs, enter due diligence, secure financing, sign definitive agreements, and close.

Most transactions finish in about 6–8 months. Complexity, size, or financing needs can extend that toward 9–12 months. Careful prep and clean records shorten time and reduce retrades.

Buyers commonly request 3–5 years of financial statements and tax returns plus bank records. They also want signed contracts, customer lists, employee documentation, and equipment logs.

To protect future cash flow and reduce risk, buyers often negotiate earn-outs, seller financing, and a transition period with seller support. These terms bridge valuation gaps and align incentives after close.

Business brokers and brokers for Main Street deals commonly charge around 10% commission. Fee models vary by deal size and can be fixed, tiered, or success-based. Higher fees reduce net proceeds, so owners should weigh wider exposure versus cost.

Key factors: disciplined preparation, clear contracts, and timely taxes improve buyer confidence and speed the sale.

Elite Exit Advisors centers its approach on earnings clarity and practical deal execution to help owners capture the full value of their firms. The team builds a sale plan that uses SDE and EBITDA metrics and current market multiples, not simple revenue rules. Elite Exit Advisors works with service-based businesses, including HVAC business valuation, HVAC business valuation, plumbing business valuation, construction business valuation, and more, to provide precise, actionable insights.

Accurate pricing starts with earnings-based methods: the firm models SDE or EBITDA depending on transferability and buyer type. That ensures pricing reflects real cash flow and comparable market multiples.

Preparation focuses on clean financials, defensible add-backs, and clear documentation for lenders and buyers. Well-packaged records shorten diligence and keep owners focused on running day-to-day operations.

Confidential outreach targets qualified buyers who can fund and close. Negotiation support aims to protect certainty at close, improve financing structure, and shape transition terms like earn-outs or seller support.

Owners see a structured process with confidentiality, staged milestones, and careful buyer screening. The goal is stronger offers, fewer retrades, and a smoother handoff with preserved value.

Elite Exit Advisors helps owners prepare for a buyer-ready exit, as they focus on clarity, credibility, and deal execution. Key support includes:

If you’re considering a sale or evaluating an offer, book a call with Elite Exit Advisors to discuss your valuation and next steps.

The strongest sale outcomes come from a tight focus on verifiable earnings and a prepared, risk‑reduction plan. Normalize results with SDE or EBITDA and back those figures with comparable sales to defend your valuation.

Buyers pay for transferable cash flow, not just revenue. Clean books, clear add‑backs, and documented contracts prove earnings and reduce buyer pushback.

Major levers that move value include contract mix, customer concentration, reliable crews, realistic equipment condition, and professional deal readiness. Timelines usually span months, so plan diligence and negotiation to protect price and terms.

Practical next step: organize financial statements and contracts, flag operational risks, and craft a concise narrative that shows how the company sustains cash. This preparation raises buyer confidence, cuts retrades, and helps reach the sale you want.