Construction business valuation is the process of determining what a construction company is worth in today’s market based on earnings, cash flow, backlog, assets, growth potential, and risk. It helps business owners understand how much they could sell for, supports buyers in making fair offers, and gives investors a clear view of financial performance and future upside. A proper valuation looks beyond revenue to factors like recurring contracts, project margins, equipment value, customer concentration, and management dependence. In practice, profitability drives price: construction businesses sell at an average 2.60x earnings multiple, with a median sale price of $750,000.

A realistic sale price starts with what a typical buyer will pay under ordinary market conditions. That idea guides how owners set expectations and prepare documentation.

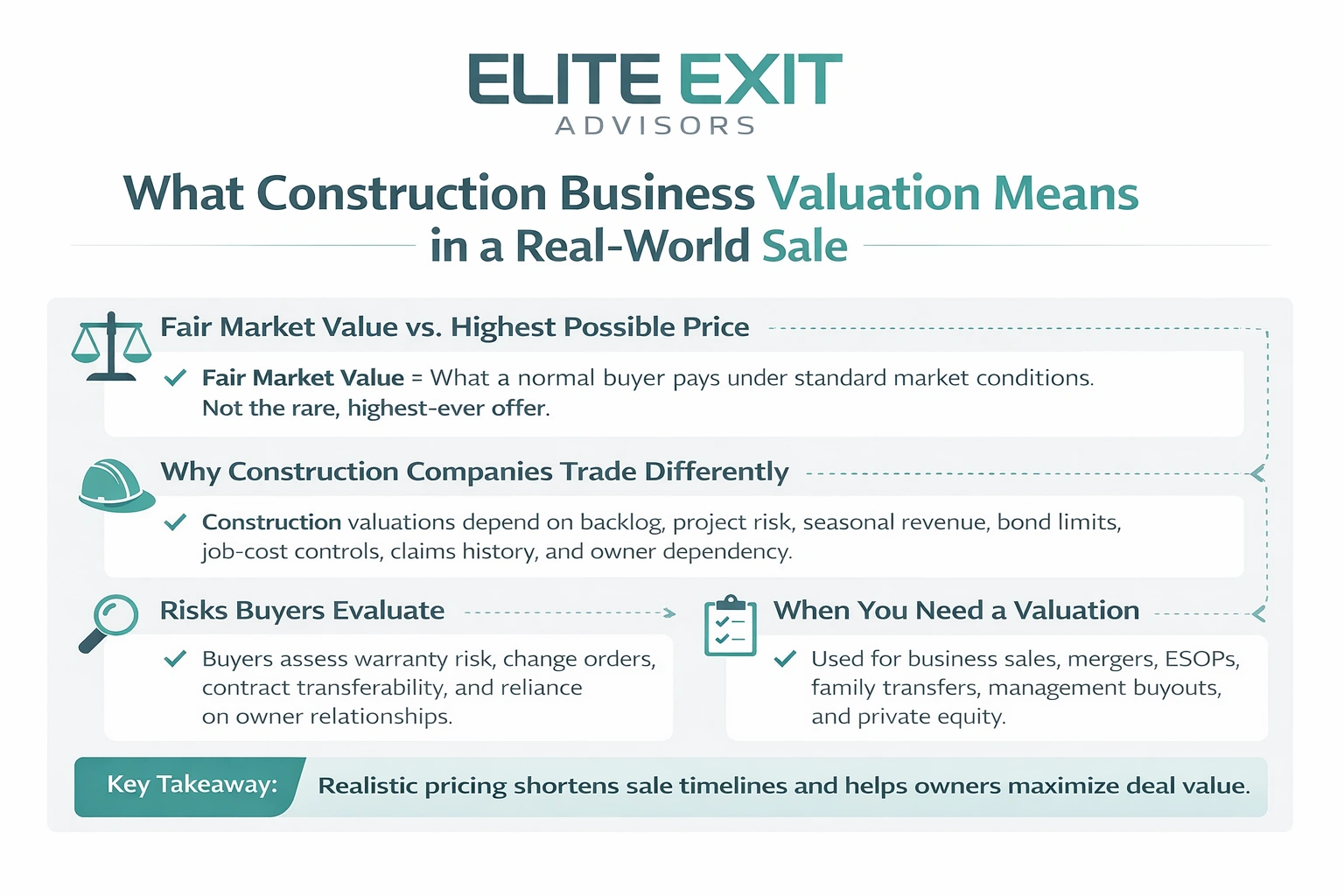

Fair market value is what a willing buyer and a willing seller agree on in a normal timeline. It is not the absolute top offer you might get in an unusual situation.

Overpricing can lead to long listing times. Underpricing can speed a sale but leave money on the table.

Project-based revenue, seasonal swings, backlog visibility, bond limits, and tight job-cost controls change how a construction company trades.

Buyers worry about claims history, warranty risk, change orders, and how tied the firm is to the owner’s relationships.

Owners often need valuations for external sales, family or trust transfers, mergers, ESOPs, management buyouts, or private equity rounds.

Valuations get simpler when you can show steady earnings and clear transferability of contracts and key relationships.

Assemble clean financial records so buyers and appraisers can trust the numbers. Begin with at least three years of tax returns and supporting statements. Year-to-date reports, job-cost detail, and clear balance sheets speed review and reduce questions.

Buyers check that reported revenue matches job performance and collections. Many firms report on a cash basis, but appraisers often convert to accrual to reveal timing gaps.

Percentage-of-completion methods can show in-process margin and over/under billings more clearly than completed-contract reporting. Those adjustments affect reported cash flow and working capital needs.

Normalize the P&L and set owner pay to market rates, remove one-off costs, and correct related-party rent or services. Separate personal expenses from company operations to show true operating income.

Working capital is often strained by retainage, deposits, and pay-when-paid clauses. Fast growth can consume cash even when the company is profitable.

Clean, explainable financials reduce perceived risk and support stronger valuations and a clearer market value outcome.

Turn reported net income into a clear, buyer-ready measure of earnings power. That bridge shows what owners actually receive and what a buyer can expect to extract after transition.

SDE typically starts with net income and adds back: interest, depreciation, amortization, owner compensation and discretionary expenses. Buyers accept these add-backs when supported by records that show they are non-operating or above-market.

Use a weighted average to smooth cycles: 50% most recent year, 37.5% prior, 12.5% third year. This reduces the distortion of an unusually strong or weak period.

Adjust for working capital swings, equipment repairs, and necessary capex. Document add-backs with invoices, payroll records, and consistent classifications to cut negotiation friction.

Credible earnings power is the foundation for choosing the right multiple in later stages of a valuation process.

Buyers focus on concrete signals that show the company can keep earning after the owner leaves. Below are the core drivers that affect market interest and deal terms.

Backlog is forward-looking proof. Signed, profitable backlog that fits current crews raises confidence.

Speculative pipeline adds little value until contracts are executable with existing resources.

Repeat customers and diversified accounts reduce risk. Heavy reliance on one client can lower multiples, even when revenue looks strong.

Owned equipment and property matter for firms that need specialized fleet. Well-maintained assets reduce buyer capex assumptions.

Intangible assets, brand, safety record, estimating skill, and vendor terms, often justify premium pricing when transferable.

Buyers pay more when supervisors, estimators, and PMs can run projects without the owner. Clear succession planning supports better deal terms.

Watch estimating accuracy, claims history, change-order discipline, litigation, and warranty exposure. These risks can compress the final value.

Appraisers rely on three principal approaches to translate cash flow, market activity, and assets into an actionable price range.

Forecast free cash flow for about five years, add a terminal value, and discount using a rate that reflects project and market risk.

Stress-test assumptions for growth, margins, and working capital to see how sensitive discounted cash flows are to realistic swings.

Normalize several years of earnings, use adjusted EBITDA or SDE, and apply a cap rate that matches stability and risk.

This method works best when past performance shows consistent margins and predictable cash extraction.

Compare multiples (EBITDA, SDE, revenue) from recent private deals, then adjust for geography, trade niche, and scale differences.

Adjust equipment and real estate to fair market levels; this method matters for asset-heavy or underperforming firms.

Compare asset-based figures to book value to expose under- or over-depreciated items, missing goodwill, and intangible factors.

Consider breakup value when selling individual assets could outstrip ongoing operations. Market capitalization applies mainly to public firms and rarely fits small contractors.

Choosing the right multiple turns reported earnings into a buyer-ready price and sets realistic seller expectations.

Revenue multiples use top-line figures and are quick checks when margins are stable. They work for repeatable contractors with predictable contracts.

Cash flow multiples (based on SDE or adjusted EBITDA) tie value to sustainable earnings. Use them when margins vary or when backlog quality is uncertain.

Market rules of thumb help frame talks: successful firms sometimes trade at about 10–30% of annual revenue. Cash flow multiples vary by niche and deal specifics. Strategic buyers can push multiples higher.

Adjust enterprise value for excess cash, subtract debt, and set working capital targets that create a true-up at close.

Quick checks: implied margin vs. historical margins, implied payback period, and alignment with backlog and customer concentration.

Ownership transfers often apply discounts for lack of control, lack of marketability, and key-person risk. These can materially lower market value in estate or minority sales.

Buyers underwrite to steady cash flow and risk. Better documentation and lower perceived risk support stronger multiples.

A strong sale outcome depends on orderly operations, clear records, and a buyer-ready narrative. Start early: get legal and operational items current, document who does what, and assemble proof of steady financial performance. These steps reduce risk and attract potential buyers who will pay more for clarity.

Complete entity documents, licenses, and insurance. Keep contract templates and a safety program on file.

Standardize estimating, job-cost controls, and delegation so projects run without the owner. This de-risks day-to-day operations and helps increase value.

Include 3–5 years of financials tied to tax returns, backlog reports, customer lists, and an org chart.

List assets, equipment, and real estate with schedules. Add photos, case studies, and references as proof of performance.

Potential buyers often include strategic competitors, adjacent trade operators, high-performing employees, and financial buyers. A broker expands reach and protects confidentiality.

.webp)

Elite Exit Advisors helps owners translate financial clarity into a practical exit plan. The team pairs forensic financial work with deal-ready storytelling. That makes market conversations smoother and reduces surprises during buyer diligence.

Elite Exit Advisors works with service-based businesses, including HVAC business valuation, HVAC business valuation, plumbing business valuation, electrical contractor business valuation, and more, to provide precise, actionable insights.

The service package focuses on clear steps rather than promises. Advisors help clarify market value, strengthen the valuation story, and prepare documentation that stands up to buyer review.

Ready to learn your company’s market options? Book a call to get a focused review and an action plan tailored to your timeline and goals.

The best exits start when owners treat valuation as ongoing management, not a one-time task. Prepare clean financials, compute sustainable earnings, assess key drivers, pick methods, and sense-check multiples so results hold up in the market.

In the construction industry, credible, transferable cash flow and low risk matter most. Backlog quality, estimating accuracy, and working capital swings often decide whether a company meets fair market expectations.

Treat this process as continuous improvement: better reporting, tighter operations, and deeper management teams raise market value over time. If you plan a sale, recapitalization, or succession, start early so changes appear in results and reduce last-minute surprises.