Plumbing business valuation is the process of estimating what a plumbing company is worth in today’s market based on earnings, cash flow, risk, and growth potential. Buyers focus far more on profitability than revenue, using earnings multiples (SDE or EBITDA) to determine a fair price. In the U.S., plumbing businesseshave a median sale price of about $620,000 and an average earnings multiple of 2.47×, showing how strongly value is tied to cash flow rather than top-line revenue

A clear estimate of what a U.S. service company could fetch on the open market guides every strategic choice an owner makes. A solid appraisal turns financials into action. It defines realistic value ranges and highlights which levers move price before going to market.

Owners use an estimate to set timing and readiness milestones. It shows what must be true operationally for a smooth transition if they choose to sell plumbing business assets or the entire company.

Buyers and lenders use the same math to compare opportunities, pick where to spend diligence time, and judge repayment risk. That makes the process a shared decision tool.

Valuation is a living process. Market conditions and company results change, so owners who track key drivers monthly avoid rushed choices and make better exits when the time comes.

Simply using a percent of top-line revenue to set price often hides crucial profit differences between firms. Owners who see a headline multiple on revenue may assume value rises as sales grow. That assumption can be false.

Imagine two plumbing firms each reporting $10M in revenue and $300k of inventory. One nets $600k after costs; the other nets $300k. Both show identical top-line figures, but the buyer who pays a revenue multiple for either will get very different returns.

Buyers underwrite deals on normalized earnings, predictable cash flow, and downside risk. They model wage inflation, vendor pricing power, and thin margins that can erode future profit.

Quick self-check: if revenue rises but margins shrink, value may not increase. Owners should watch profits, not just sales.

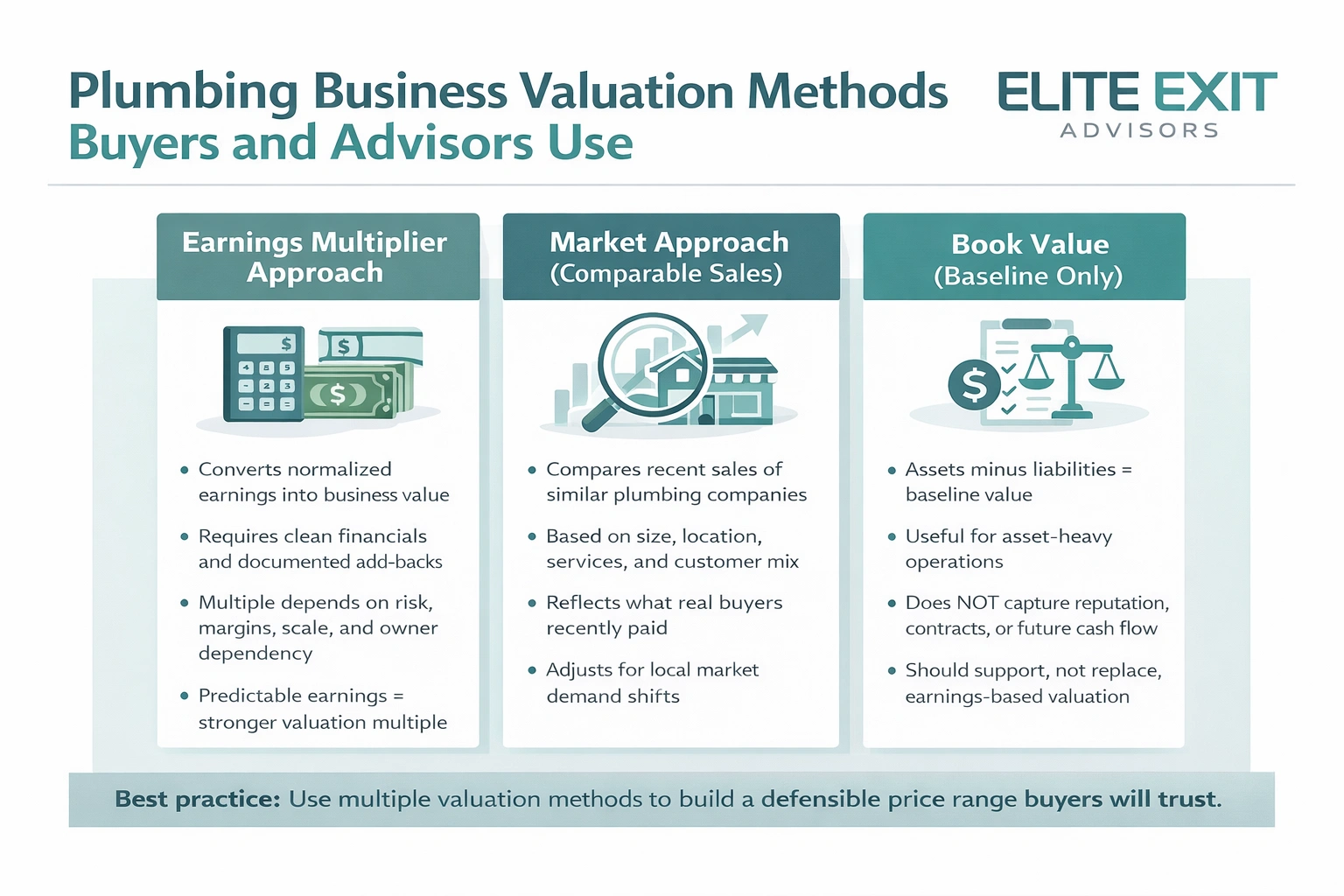

Advisors rely on several established approaches to estimate what a service company will command on the open market. Using more than one method helps buyers and sellers spot gaps and build a defensible price range.

The earnings multiplier converts normalized earnings into value. Clean financials and documenting add-backs to reach a repeatable earnings number.

Then apply a multiple that reflects risk, scale, margins, and local demand. Higher predictable earnings and low owner dependency justify stronger multiples.

This method compares recent sales of similar companies by size, geography, service mix, and customer profile. It helps set a realistic multiple range tied to what active buyers actually paid.

Comparable sales fill gaps the earnings method can miss, especially when local market appetite shifts rapidly.

Book value equals assets minus liabilities. It is useful for asset-heavy operations but omits intangibles like reputation, contracts, and future cash flow.

Buyers will pressure-test whichever method yields the highest result, so consistency across approaches matters.

Practical next step: prepare buyer-ready financials and a defensible normalization schedule before applying these methods.

Assemble the records that prove your company’s recent financial story. Well-organized files help buyers move faster and reduce price uncertainty.

Checklist: provide 3–5 years of P&Ls, balance sheets, and signed tax returns, plus an interim year-to-date package that ties to bank statements.

Tax returns matter because lenders and many buyers use them to confirm earnings. They cut disputes over reported profit and make underwriting smoother.

Document service lines (repair, install, remodel), job costing, average ticket, and revenue split by residential, commercial, and property management clients.

Show customer concentration, list top clients, and attach any recurring contracts; recurring work signals stability in the customer base.

Provide an assets schedule, inventory practices, and a fleet list with ages and replacement cycles. Note equipment condition and major upcoming capital needs.

Also disclose all liabilities: debt, leases, unpaid taxes, and contingent exposures. Clear documentation reduces unknowns and supports stronger pricing conversations.

A clean picture of recurring profit begins when you remove personal and unusual costs from reported results. Normalized earnings show what the core operation generates after excluding items that do not reflect ongoing performance.

Buyers often accept documented personal costs that the seller charged to the company. Typical examples include personal auto usage, cell phone bills, travel for nonwork reasons, and personal memberships.

Provide receipts or a clear policy tying these items to the owner. Credible support speeds the underwriting process and preserves offer strength.

One-time legal settlements, unusual repairs after a storm, or an extraordinary recruiting fee are usually removed from normalized earnings. These items do not show ongoing cash flow.

Be careful: items labeled “one-time” but that repeat annually will be challenged and likely rejected.

Adding back interest, taxes, depreciation, and amortization helps compare firms with different financing or accounting choices.

Owner salary matters: SDE models often add back full owner compensation to show seller discretionary benefit, while EBITDA frameworks may only adjust excess owner pay. The chosen metric drives acceptable add-backs and the multiple range buyers will apply.

SDE translates the company’s reported profit into the real money an owner keeps or controls each year. It shows the total annual economic benefit for one full-time owner-operator.

SDE equals net income plus things the owner benefits from but a buyer would not pay for after the sale. It reflects true cash flow available to an individual owner.

Use SDE for smaller, owner-led firms where a buyer will run day-to-day operations. It helps a buyer estimate how much cash they can extract when they step in.

They look for consistent add-backs, bank or card proof, and reasonableness versus norms. Lenders check whether an expense truly disappears after sale.

Realism check: if SDE depends on extreme owner hours, buyers may cut the multiple. Documenting SDE clearly helps owners support price and reduce late-stage renegotiation when they aim to value plumbing business or to value plumbing business assets for sale.

A company with repeatable management practices is usually judged by EBITDA rather than the owner’s take-home pay. EBITDA isolates operating earnings before financing and non-cash charges, so buyers can compare firms on a like-for-like basis.

Buyers shift to EBITDA as earnings grow and a management team runs daily operations. At that point, underwriting focuses on company-level cash flow instead of owner benefit.

Buyers typically add back only excess owner salary above a market replacement. They estimate what a qualified manager would earn and treat the remainder as an add-back to earnings.

EBITDA usually produces a lower figure than SDE because owner salary treatment changes. Still, larger firms can command higher multiples due to scale, lower perceived risk, and easier financing.

Multiples reflect risk, market momentum, and the quality of earnings. The next section explains how multiples are set and what moves them up or down in the market.

Multiples translate current profits into a market price. They offer a quick way for buyers to express confidence in future cash flow. A well-supported multiple reflects both measurable results and risk perceptions.

Higher, consistent earnings usually raise the multiple a buyer will pay. Key risk factors that push multiples down include heavy owner dependence, tight customer concentration, inconsistent margins, weak records, and staffing gaps.

The home services market is fragmented but consolidating. That trend boosts buyer interest and can lift multiples as strategic buyers seek roll-up growth. At the same time, increased competition raises expectations for systems and professionalism.

Larger companies often earn higher multiples because scale lowers perceived risk. Strong systems, diversified customers, and leadership depth make growth easier to underwrite. Higher earnings allow more debt capacity and widen the pool of buyers.

Predictable income from maintenance plans and low customer concentration reduce deal risk for buyers. Below are the practical factors that raise buyer confidence and price.

Service agreements and maintenance plans boost retention and smooth cash flow. Buyers want clear terms, renewal rates, and churn metrics. Well-documented contracts with auto-renew or notice windows are ideal.

A varied customer base limits downside if a large client departs. Buyers discount companies with a single client making up a big share of revenue.

Consistent reviews, fast responses, and local search presence cut marketing costs. Reputation drives homeowner trust and steady lead flow.

Buyers pay more when day-to-day sales and dispatch run without the owner. Multiple licensed technicians and trained staff reduce compliance and continuity risk.

Disciplined pricing, job-cost tracking, and the ability to pass on cost increases protect margins. Documented expansion plans, new services, or eco-focused upgrades show realistic growth potential.

Who will buy your company depends on size, systems, and how the owner fits in the day-to-day. As earnings and operational depth grow, the most likely buyer moves from an individual operator to a strategic consolidator or institutional buyer.

Individual buyers often plan to run the company themselves. They rely on lender approval, so clean financials and clear payroll matter.

Seller transition support and documented training can improve deal terms and shorten lender review.

Strategic buyers look for route density, recurring customers, and branding that fits their footprint.

They pay more for operational synergies and a clear path to increase margins through cross-selling.

Private equity groups require tight reporting, strong management, and scalable processes. They want a repeatable growth story and professional controls.

Without an experienced leadership team, institutional buyers lower offers or walk away.

Takeaway: Align documentation and operations to the buyer pool you expect. That focus helps you pick the right earnings metric, tighten diligence, and present a credible path to value.

Follow these steps to move from raw earnings to a defensible asking price. The goal is a repeatable process you can test before speaking with buyers or lenders.

Select SDE if an owner runs daily ops. Pick EBITDA if management runs the firm. The choice changes acceptable add-backs and the multiple a buyer will apply.

Create an add-back schedule and attach evidence: invoices, payroll records, and bank statements. Keep explanations short and specific so lenders can verify quickly.

Use local comps to form a range, not a single high number. Adjust the multiple for size, margin, and risk rather than cherry-picking the top sale.

Subtract outstanding debt and factor in working capital needs. Decide which assets (vehicles, inventory, equipment) transfer and how that affects net proceeds.

Set an asking price above the mid-point and a target below it. Anticipate diligence cuts for unsupported add-backs or weak records.

.webp)

Small, targeted steps taken now often boost sale outcomes more than last-minute fixes. Focus on actions buyers reward: lower risk, reliable recurring income, and operations a new owner can run without the founder.

Create service agreements and maintenance plans that convert one-off work into steady revenue. Price plans to show clear annual renewal rates and record churn monthly.

Delegate estimating and sales tasks to trained staff. Document standard operating procedures and measure weekly KPIs so performance is independent of any single person.

Keep multiple licensed leaders on staff and build a technician pipeline. Show retention rates and training schedules to prove continuity and reduce buyer concern.

Standardize communication, shorten scheduling windows, and publish warranty policies. Track review volume and close rates to show measurable marketing and service gains.

Present a short plan with past trends, key leading indicators, and realistic initiatives (new services or nearby expansion), including costs and projected impact over 12 months.

Diligence is where paperwork and reality meet, and where many deals slow or fall apart. Early preparation preserves value, keeps momentum, and reduces renegotiation risk during a sale.

Organize all contracts, recurring service agreements, and warranty terms so a buyer can verify recurring revenue and liability exposure quickly.

Provide staff lists, licenses, training logs, payroll records, and contractor status. Buyers focus on licensing gaps and labor risk.

Maintain maintenance logs, titles or lease agreements, safety policies, and inventory controls. These items prove operational discipline and protect assets.

Reconcile P&L to tax returns, tie add-backs to receipts, and ensure bank statements match reported cash flow. Unsupported items become negotiation targets.

Experienced advisors focus attention on the few items that most often erode price during diligence. Elite Exit Advisors works with service-based businesses, including HVAC business valuation, HVAC business valuation, landscaping business valuation, and more, to provide precise, actionable insights. That range drives a focused plan to improve earnings quality, reduce risk, and match the right buyers.

.webp)

Owners who prepare get clearer ranges, fewer surprises in diligence, and stronger negotiation leverage at sale. Book a confidential call with Elite Exit Advisors to discuss goals, timing, and what buyers are likely to pay for your specific plumbing company in the U.S. market.

A clear, earnings-based estimate gives owners a practical roadmap for action, not just a headline price. A solid plumbing business valuation rests on SDE or EBITDA and on records that buyers can verify. Credible numbers hold value through diligence.

Follow a simple process: gather financials, normalize earnings, pick SDE or EBITDA, apply a realistic multiple, then adjust for working capital, debt, and asset transfers before setting an asking range.

Multiples move with risk and operational strength, so targeted improvements often raise value more than quick fixes. Treat valuation as a planning tool to set priorities and timelines.

Use the checklists in this guide to spot gaps. When you’re ready for a formal review or exit plan, consider a confidential conversation with Elite Exit Advisors to map next steps.