Seller’s Discretionary Earnings (SDE) is a straightforward way to show total owner benefit for many small to mid-sized firms. It normalizes profit, as it adds back owner pay, perks, and one-time items. That makes it a quick proxy for free cash flow when buyers and lenders review a company.

This approach is especially common in smaller transactions; industry data shows that around 75% of businesses valued under $500,000 rely on SDE as the primary earnings metric, with usage still dominant in deals up to $1 million. That widespread adoption reflects how well SDE captures real economic benefit in owner-run companies, making it a practical proxy for cash flow when buyers and lenders evaluate value, affordability, and risk.

SDE in business defines the normalized profit an owner actually keeps after adjusting for salary, perks, and one-time expenses. For many U.S. owner-operated firms, this metric approximates free cash flow and shows the true economic benefit an owner receives.

Discretionary earnings start with pre-tax profit and add back owner compensation, non-operating items, interest, depreciation, and one-offs. The result estimates what a buyer-operator might expect to extract as personal payout.

Owners often pay themselves a salary, run personal expenses through the company, or take extra benefits. Adding those items back converts accounting profit into a total owner benefit figure that reflects real economic gain.

Clear rules for add-backs and exclusions keep valuations consistent. Separate recurring operating results from owner-specific or one-off items. That helps buyers compare historical figures across similar firms.

Income taxes vary by owner and entity. Excluding them lets buyers view earnings regardless of tax choices.

Interest reflects capital structure. Adding it back removes financing differences from operating performance.

Depreciation and amortization are non-cash charges. Restoring them shows cash available to a new operator.

Owner salary, payroll taxes, and personal benefits often get added back. Above-market pay or personal expenses run through the company boost reported costs and reduce apparent earnings.

Discretionary expenses are optional owner choices. Operating costs are needed to run operations. Mislabeling either type commonly triggers questions during diligence.

One-time items like major legal settlements, an unusual consulting project, or a rare bad debt should be normalized. Buyers remove these to see sustainable earnings performance.

Tip: Document each add-back with support to make adjustments defensible.

Begin the process with pre-tax income (EBT) and reconcile that figure to tax returns and the general ledger. Working from EBT keeps the calculation traceable to official records.

Use the reported EBT as your anchor. Confirm totals on profit and loss statements match recent tax filings so the rest of the calculation reconciles cleanly.

Adjust owner salary to a market, replacement-cost level, including payroll taxes. Buyers focus on what a new operator would reasonably pay a manager, so document any under- or overpayment.

Add depreciation and amortization back to EBT. These are non-cash items, though buyers will still assess future capital needs separately.

Add back interest expense on a net basis (interest expense less interest income). This removes capital structure differences across firms.

Review general ledger lines for travel, meals, memberships, vehicle costs, and health insurance. Treat mixed-use items conservatively and document allocation. Adjust for legal, consulting, or bad debt that clearly occurred only once.

Final note: The best calculation balances useful add-backs with defensible adjustments supported by records so reported earnings reflect true owner benefit.

A clear formula restores owner pay, interest, D&A, and selective expenses to show true operator cash flow.

Formula: SDE = Pre-Tax Income (EBT) + Owner’s Salary + Interest Expense (net) + Depreciation & Amortization + Discretionary Expenses + Non-Recurring Expenses.

Each add-back removes items that mask the company’s usable profit.

Typical items found on small U.S. records include travel, meals, health insurance, personal vehicle costs, family payroll, and owner perks.

An add-back is legitimate when it does not reflect necessary operating cost for a replacement owner. If the cost must continue to run the company, buyers will often reject it.

We’ll convert a set of real LTM figures into a single adjusted earnings total so you can map the steps to your own records.

Why each add-back matters: owner pay shows replacement cost; net interest removes capital structure; D&A restores non-cash items; discretionary and one-offs show sustainable profit. Buyers then apply a multiple, test debt service coverage, and compare to expected owner cash flow.

Limitation: This adjusted total is a useful profit proxy but not true cash flow. It excludes capex, principal debt payments, and working capital changes that affect available cash.

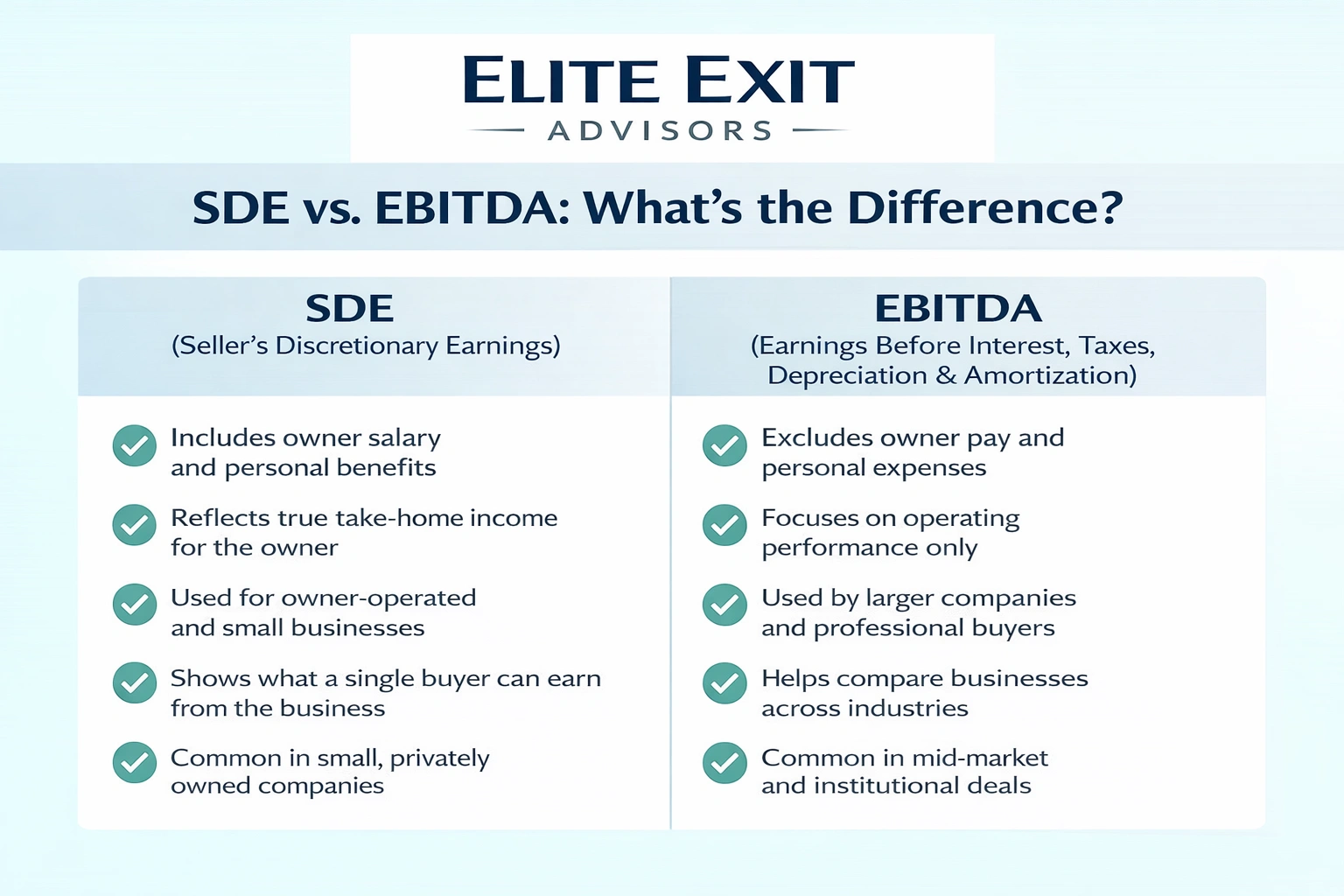

Choosing the right earnings metric depends on the owner’s role and how compensation appears in the financials. For owner-operated businesses, SDE vs EBITDA serves different purposes. SDE captures personal pay and discretionary benefits, reflecting the true economic return to the owner, while EBITDA focuses on operating performance independent of ownership. Larger companies typically rely on EBITDA, while smaller, owner-run firms lean on SDE to show real-world earning power.

Owner salary and perks drive the core difference between sde and ebitda. Seller discretionary earnings add back the owner’s total take, including personal expenses run through the company. EBITDA leaves management pay as an operating cost, so it understates owner benefit for small firms.

Buyers evaluating an owner-operated company usually favor sde because it reflects transferable cash to a new operator.

By contrast, larger strategic buyers and lenders often use ebitda or adjusted ebitda to compare across firms with professional management teams.

Valuation impact: Choice of metric changes multiples, affects comparables in the market, and influences lender comfort. Pick the measure that matches company structure so buyers see realistic earnings and deal math aligns with valuation expectations.

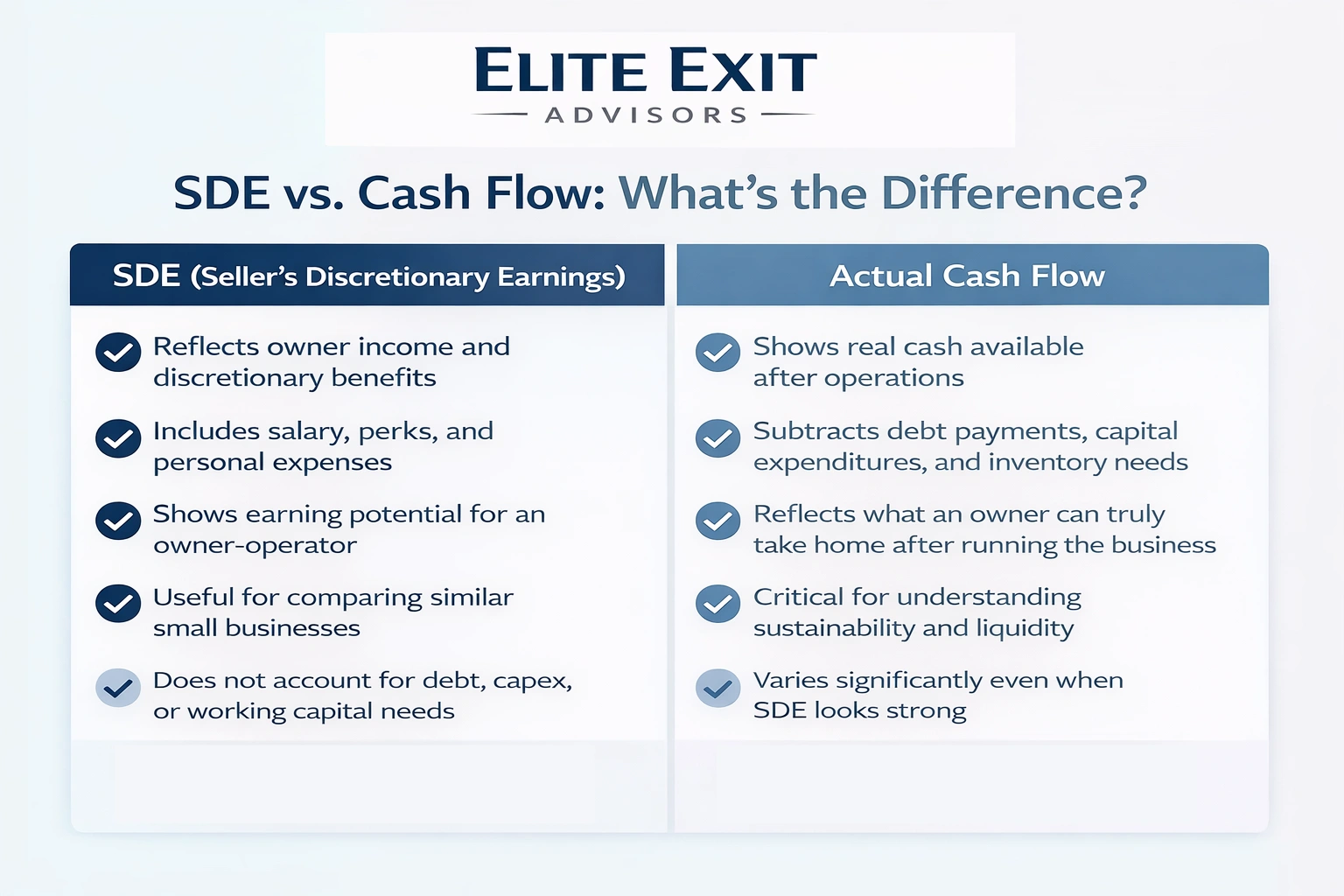

SDE often serves as a quick proxy for owner cash generation, but it does not show every drain on available funds. For owner-operated firms, this metric captures owner pay and discretionary expenses that flow back to the person running operations.

Because owners frequently extract value through salary and perks, seller discretionary and discretionary earnings track real payouts. Buyers use that figure to gauge prospective owner profit and to compare similar companies.

SDE does not include capital expenditures, principal debt repayment, or swings in inventory and receivables. Each of these items can materially reduce real cash available after a sale.

Practical conversion looks like: SDE minus debt service, minus a capex reserve, minus working capital needs. Two firms with identical SDE can feel very different if one needs major equipment replacement or tight inventory cycles.

Bottom line: pair seller discretionary figures with cash flow statements, bank activity, and a realistic post-close plan so buyer expectations match likely owner cash access.

Market multiples applied to normalized earnings form the usual route from recorded profit to suggested sale price. Document adjusted seller discretionary earnings, then apply a market multiple to produce an indicated valuation range.

Buyers review normalized earnings, compare market multiples, and derive an offer range. A clean earnings record often narrows that range and speeds closing.

Real operational gains and well-documented add-backs justify a stronger asking price. Fewer disputed adjustments reduce the chance of discounts during diligence.

Buyers use earnings to estimate payback and risk. Lenders lean on coverage ratios tied to adjusted earnings to test debt service capacity.

Compare your earnings profile to similar sellers in the market to see if your valuation stands up. A defensible story limits renegotiation and raises buyer confidence at LOI and final terms.

Minor add-back mistakes often trigger major price adjustments when buyers dig deeper. During diligence, credibility matters more than optimistic totals. Poor choices on adjustments or weak documentation alert buyers and reduce valuation.

Labeling personal travel, club dues, or family payroll as operating expenses erodes trust. Buyers will question discretionary earnings when receipts and memos are missing.

Not setting related-party rent or owner salary to market levels skews profit. These non-arm’s-length arrangements make valuation comparisons unreliable.

Missing invoices, messy GL codes, and late tax filings slow review. Delays increase perceived risk and invite price renegotiation by buyers.

One-time costs left in place understate earnings. Conversely, excluding recurring problems overstates value. Buyers expect clear rules for each adjustment.

A clear, repeatable earnings story shortens due diligence and strengthens negotiation leverage.

Elite Exit Advisors focuses on earnings quality, clean financial presentation, and operational clarity. That makes seller figures clearer to buyers and lenders.

We run a structured prep process to identify discretionary items, validate add-backs, and link each adjustment to source documents.

Engagement outcomes include a clearer understanding of owner benefits and cleaner categorization of expenses. Those changes help your valuation and diligence health.

Elite Exit Advisors helps you create a clear SDE story, reviews your financials and separates true operating expenses from discretionary spending.

Book a call with Elite Exit Advisors to get a clear, defensible SDE narrative and a practical plan to improve earnings quality before you go to market.

Center your sale story on normalized owner earnings. Treat seller discretionary earnings as the practical measure that shows owner-operator payout and guides valuation for many small companies.

Calculate from EBT with clear add-backs: owner compensation, net interest, D&A, discretionary expenses, and non-recurring items. Keep each adjustment documented and repeatable so buyers trust the numbers.

Remember the difference versus EBITDA and true cash flow: adjusted earnings show owner benefit but do not replace capex, debt service, or working capital analysis. Use SDE and discretionary earnings as both metric and communication tool to influence value and negotiation outcomes.

Next step: review the last 12 months of financials, build a clean add-back schedule, and align earnings interest and other adjustments with supporting evidence before entering sales. Consider help from Elite Exit Advisors if you want a defensible valuation approach.