Typical U.S. commissions that brokers charge to sell a business range from 5% to 15%, with many smaller deals clustering near 10%. Fees are most often success-based and are paid from proceeds at closing.

Working with a broker can materially influence both the final sale price and the overall outcome of a transaction. The real value comes from how effectively the broker positions the business, sets realistic pricing, and determines how much a business can sell for in the current U.S. market. Strong representation helps owners move beyond surface-level fees, focus on net proceeds, avoid costly mistakes, and reach a sale price that reflects true market demand rather than guesswork.

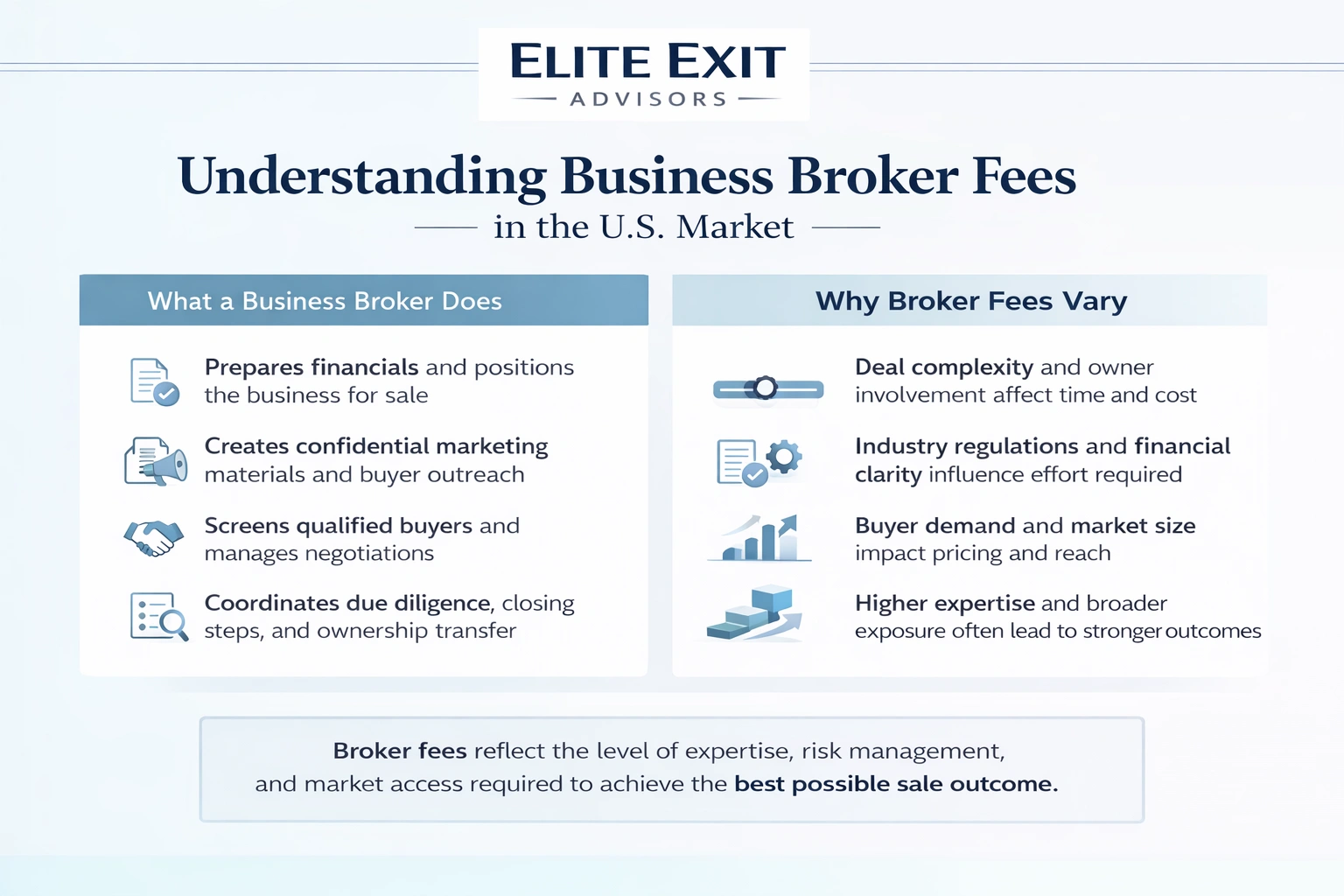

A smooth sale depends on a clear process and skilled guidance. A business broker helps owners prepare value claims, craft marketing materials, and contact qualified buyers. That support reduces risk and keeps sensitive details confidential while widening reach.

Fee levels reflect scope and complexity. Deals with heavy owner involvement, customer concentration, weak records, or strict regulation need more time and expertise. That raises fees.

Useful drivers include timeline expectations, record quality, buyer pool size, and sector rules. Fees pay for process management that cuts mistakes and can lift final value. A broker’s experience and marketing reach often matter as much as the commission rate when choosing representation.

Commission levels in the U.S. depend on sale price and complexity. Commonly cited ranges sit between 5% and 15% of final sale price. For many small transactions, the midpoint near 10% is typical.

Smaller price bands tend to carry higher percentages because the work required is similar regardless of price. Larger deals can support lower percentages as value rises and the seller pool broadens.

An average commission of roughly 10% normally funds valuation guidance, creation of a marketing package, buyer sourcing, negotiations, and closing coordination. This single fee often replaces multiple hourly costs and keeps the process aligned with closing success.

Many tasks are fixed effort: preparing financials, vetting buyers, and running due diligence. When sale price is low, those fixed costs raise the effective percentage a seller pays.

Fee arrangements matter. Knowing common models helps owners compare offers and predict net proceeds.

Most common: a success fee is a percentage taken from sale proceeds at closing. This aligns incentives since payment follows a completed transaction. Sellers get focused effort without large upfront payouts.

Some brokers require a listing or engagement fee for valuation work and marketing materials. These may cover teasers, buyer research, and initial outreach. Check whether that amount will be credited against the success fee.

Complex transactions sometimes use monthly retainers. Ongoing work can include expanded outreach, heavier diligence coordination, and multi‑party negotiation support. Retainers are often credited back at closing.

Minimum commissions protect firms on very small transactions. If a percent would yield a low figure, a fixed minimum triggers. Know the trigger point and run the math against expected price.

Scaled rates fall as price rises. Reverse‑scaled gives lower rates on lower tranches. Fixed fees set one predictable cost regardless of final price. Review the listing agreement for exact triggers and credit rules.

The fee profile depends largely on company scale and the final sale price, not just the percent quoted. Identifying your size band helps anticipate commission mechanics, retainers, and minimums. Below we define three practical bands and what sellers usually see in each.

Main Street firms (often under $1M revenue) commonly face an effective percentage near 8%–10% of sale price. Minimum commissions often sit around $10,000–$15,000.

Retainers are less common at this level because most firms prefer success‑only models and simpler outreach.

Lower middle market transactions use tiered formulas such as Double Lehman: 10% on the first $1M, 8% on the next, 6% next, 4% next, and 2% above $4M. This structure balances effort across tranches and scales commission as price rises.

Minimums here often range $35,000–$50,000 because the process demands broader buyer outreach and more diligence coordination.

Middle market deals typically see lower success fees, roughly 1%–4%, since sale price is higher and work scales differently. These engagements usually include retainers that run from $5,000 up to $50,000+ depending on complexity.

Industry rules, valuation quality, and regulatory needs can still raise or lower the quoted rate within each band.

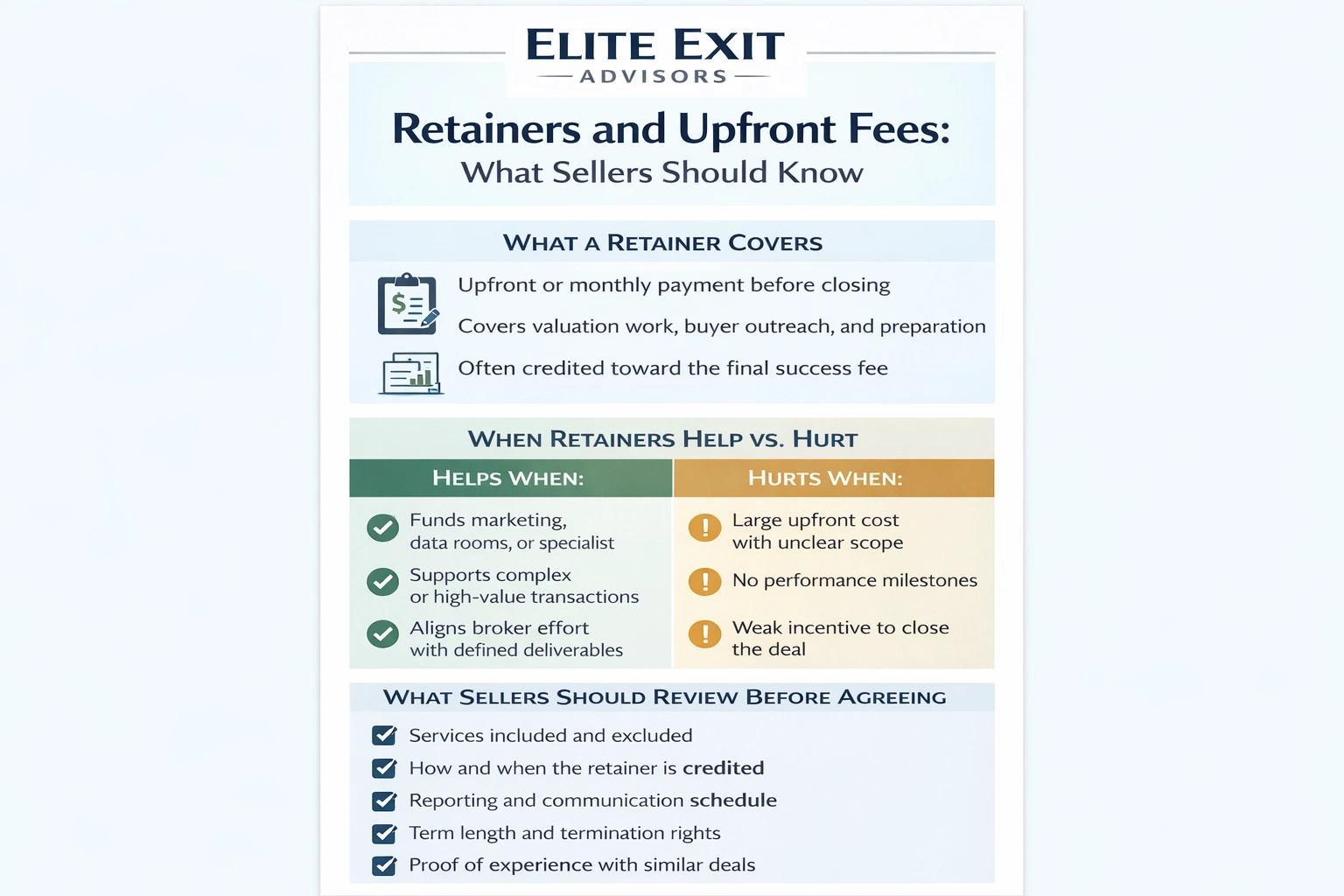

Upfront payments can fund initial valuation work and targeted buyer outreach. A retainer is an upfront or monthly payment that covers real costs before closing. In many U.S. engagements the amount is credited against the final success fee at closing.

Typical ranges vary widely. Expect figures commonly cited between $5,000 and $50,000+. The spread reflects deal scope, required marketing, and specialist advisors needed on complex transactions.

Retainers help when they pay for costly marketing, data rooms, or niche outreach that otherwise stalls progress. They can hurt when large upfront sums reduce the broker’s urgency and misalign incentives.

A clear split between included services and external expenses helps owners budget realistically. Know which tasks the broker will handle and which require outside professionals.

Most firms provide pricing guidance or an opinion of value as part of the standard fee. This helps set expectations for the marketplace.

Formal valuation reports cost extra and matter for larger, complex, or contested transactions. Expect higher fees for third‑party appraisal work when lenders or litigators require proof of value.

Legal drafting, tax planning, accounting reviews, and quality‑of‑earnings reports are usually outside the fee. These items can range from a few thousand dollars up to tens of thousands for complex industry or regulatory cases.

Avoid surprise bills: define roles early, confirm which advisor handles each deliverable, and require written lists of excluded costs. The true cost of a sale equals the broker fee plus professional fees and any cleanup work needed to present solid financials.

Sellers face a mix of operational, market, and regulatory drivers that affect fee quotes and timing. Use this checklist to gauge where your company will sit on a spectrum from simple to complex.

Complex deals require more time. Heavy diligence, earnouts, or special approvals raise the broker's workload and total costs. Regulated industries often need legal and permit work that lengthens the timeline and increases fees.

Profit quality, stable cash flow, recurring revenue, and a diverse customer base boost buyer interest. High customer concentration or unstable margins reduce demand and can raise the quoted fee or minimum.

Companies that run without the owner attract more buyers and close faster. Strong marketing and co‑broker networks widen the pool of potential buyers but add execution costs that often improve sale price.

Self‑assessment: Simple (clean records, steady profit), Moderate (some concentration, limited owner independence), Complex (regulation, earnouts, poor records).

Sellers typically defer payments until closing so costs come from sale proceeds. This preserves cash during the process and aligns incentives: the broker earns payment only when a transaction completes.

A seller hires a broker to run the sale and represent seller interests. The standard flow takes the broker fee from proceeds at closing, which reduces upfront burden. Define payment timing and outcomes in writing so there are no surprises if a deal falls apart.

Co‑brokering shares fees with another firm and widens access to buyers. Confirm confidentiality steps and the exact split before signing. Wider exposure often speeds the process while protecting sensitive details.

Agreement review checklist: confirm services, reporting cadence, buyer qualification standards, termination terms, and confidentiality measures before signing.

Picking the right rep starts with clear comparison, not a single percent. Request standard proposals from three firms and insist on the same format. That makes quotes comparable and highlights real differences in scope and timing.

Ask each firm for: scope, exclusions, timing of payments, and any minimum fee. Put answers in a simple table so you can compare line by line.

Check relevant industry experience and similar‑size closed deals. Confirm buyer sourcing method, sample marketing materials, and reporting cadence. Talk with references.

Watch for vague marketing plans, hidden charges, weak buyer screening, or unclear process ownership. Before signing, request a sample timeline, deliverables list, and two references.

Focus on net proceeds, certainty of closing, and timeline rather than the lowest rate. The right partner often pays for itself in value and speed.

Elite Exit Advisors frame each engagement around measurable results and clear timelines. Owners keep running operations while an experienced team manages outreach, negotiations, and closing readiness.

If you want clear fee expectations, realistic timelines, and a go‑to‑market plan, book a confidential call with Elite Exit Advisors for tailored guidance and next steps.

Selling with broker help usually means balancing percentage fees against the value and certainty a professional process delivers.

Core benchmarks: U.S. commissions commonly sit between 5% and 15%, with roughly 10% typical for smaller deals. Retainers or upfront fees may apply and should align with deliverables.

Recognize main fee models: success fee at closing, minimum commissions, sliding scales, and occasional retainers. Size and complexity shape final pricing and timelines.

Budget for extra costs: legal, accounting, and formal valuation often sit outside broker fees. Use earlier checklists and questions when comparing offers.

Next step: prepare basic financials, clarify exit goals, then discuss options with a qualified business broker or advisor before finalizing plans.