.webp)

Business valuation for an exit strategy is the structured process of assessing your company’s current worth with a future sale or transition in mind. Unlike a rule-of-thumb business valuation, which relies on simple multiples or rough estimates, a formal valuation shows what buyers are willing to pay, what goals are realistically achievable, and which gaps need addressing well before a sale. Without this objective baseline, owners often misprice their business, give up value during negotiations, or feel pressured into suboptimal deals.

In fact, only 20–30% of businesses that come to market successfully sell, largely because many owners enter the process unprepared and without a valuation-driven plan.

A comprehensive valuation provides clarity on true value drivers, identifies areas for improvement, and ensures your personal financial objectives align with market realities. Below, we’ll explore the valuation process, the key factors buyers focus on, and how to leverage valuation as the engine of a strategic exit plan.

Many owners discover that a planned sale can arrive overnight when personal or market shocks change timing. That reality makes an early assessment essential rather than optional.

Real-life triggers, health, a key employee leaving, or an unsolicited offer, compress timelines. Owners who wait lose negotiating leverage and miss time to fix weak spots.

An exit valuation is the estimated worth at the moment of a transaction, not a casual guess. It draws on audited financials, normalized cash flow, assets and liabilities, and industry trends.

Think of valuation as a starting point: a working number that evolves as market conditions and performance change.

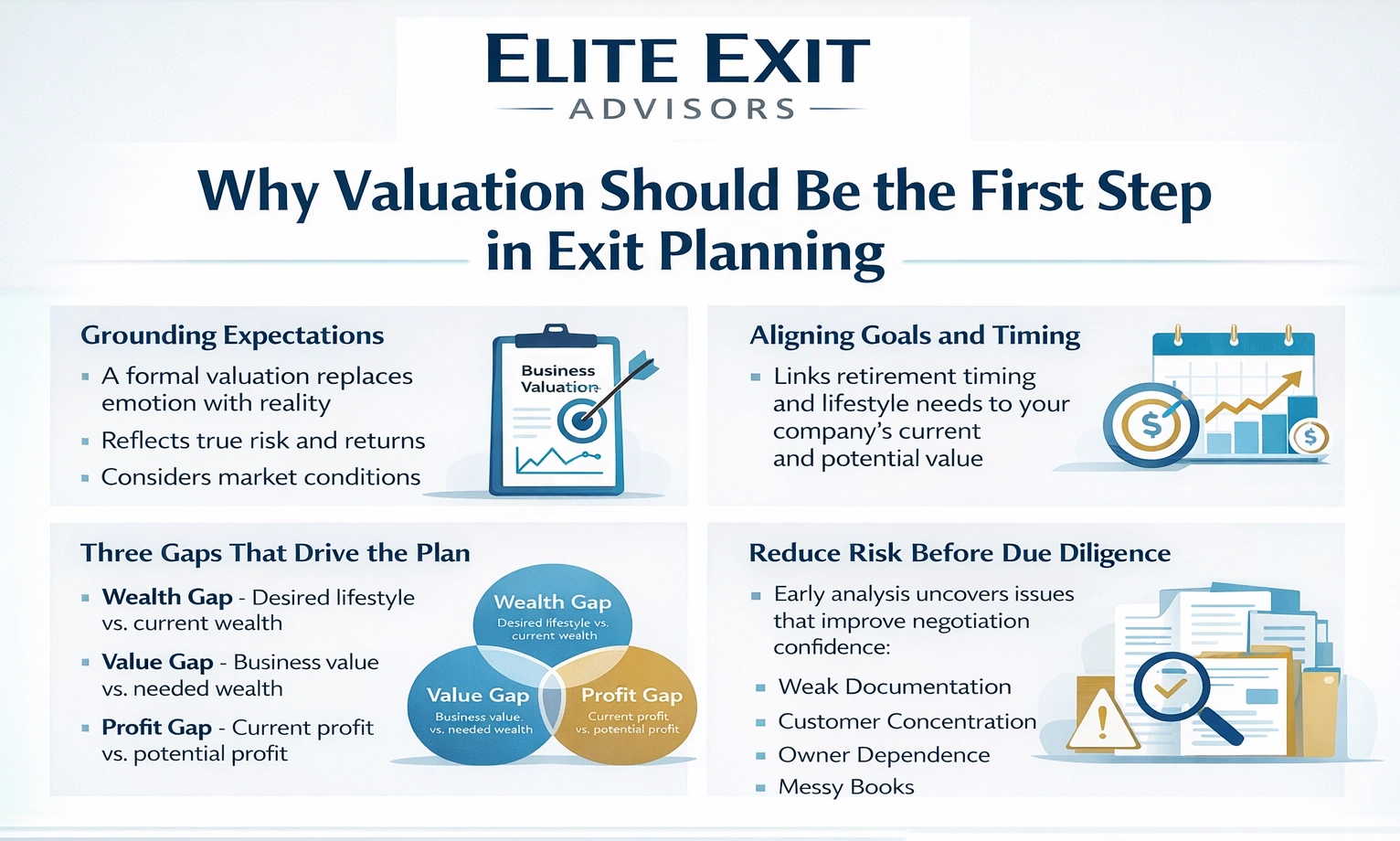

A sudden shift in personal plans or a change in demand can make an owner need a firm number far sooner than they expect. A formal appraisal belongs at the front of planning because it anchors every major decision that follows.

Grounding expectations: An objective market number replaces emotion with reality. It folds risk, return expectations, and current deal conditions into a single defensible view.

A clear estimate links retirement timing and lifestyle needs to what the company can deliver today and after improvements. That alignment reveals practical opportunities and limits.

Early analysis surfaces weak documentation, customer concentration, owner dependence, and messy books. Fixing these takes years, not weeks, and raises confidence in negotiations.

Potential buyers dig past headline revenue to test how durable cash generation really is. They want evidence that profits and systems will survive a change in ownership. This assessment shapes deal terms and confidence to close.

Buyers study cash flow stability, margin trends, and the repeatability of earnings. Clean records, few one-time add‑backs, and transparent reporting signal reliable profit.

Heavy reliance on one or two clients raises risk. That concentration often triggers holdbacks, earnouts, or tougher reps and warranties during negotiation.

Market positioning matters: differentiation, pricing power, and defensible margins show a company can withstand competitors and protect returns.

Documented processes, clear KPIs, and capable middle management reduce owner risk. Buyers pay more when operations run without daily owner input.

Buyers underwrite growth, as they link projections to capacity, demand, and systems, not optimism. Credible plans boost both price and certainty of close.

A handful of measurable items drive how a buyer values performance and risk. Each factor can shift not only price but also how much cash appears at close, whether seller financing is needed, or if earnouts and holdbacks appear in the terms.

Consistent revenue and stable margins support higher multiples and cleaner deal terms. Volatile earnings force buyers to add protections like earnouts or larger holdbacks.

When capital is plentiful and buyer demand is high, valuations rise. In tight markets, rates climb, multiples compress, and more seller financing may be required.

A deep management team reduces transition risk. Strong leadership often converts into more cash at close and fewer contingent structures.

Durable advantages, niche dominance, switching costs, or a strong reputation, preserve margins and increase transferable value.

Transferable value hinges less on spreadsheets and more on four core forms of capital. These intangible drivers often matter as much as cash flow when buyers judge risk and upside.

Strong leadership and clear roles reduce founder dependence and boost buyer confidence. Hire deputies, document decisions, and train teams to keep momentum after a sale.

Durable contracts, diversified accounts, and repeat revenue raise perceived worth. A healthy mix of clients lowers concessions and earnouts during negotiations.

Repeatable processes, clean reporting, and usable IT make operations easy to transfer and scale. Standardized playbooks help business continuity and reduce friction.

Low turnover, shared values, and internal trust cut integration risk. Preserve retention plans and clear communication to protect morale and deal certainty.

Practical steps: strengthen bench roles, formalize contracts, codify procedures, and invest in culture to protect value and create more opportunities for a smooth transfer.

Different appraisal approaches spotlight cash generation, market evidence, or net assets, none tells the whole story alone. Professionals often run several methods to triangulate a defensible range that holds up in negotiation.

The discounted cash flow (DCF) approach projects future cash flow and discounts those amounts to present value using a rate that reflects risk and time. It works best when earnings are predictable and you can justify growth assumptions.

Market-based methods use comparable transactions and industry multiples to anchor price expectations. They provide real-world pricing signals and are useful when there are recent, similar deals to reference.

Asset-based measures total tangible and intangible assets minus liabilities. This approach fits asset-heavy operations, underperforming companies, or wind-down scenarios where liquidation value matters.

Walking through hard numbers and market signals turns a vague estimate into an actionable plan. The process starts with a focused review of recent performance and ends with clear timing and deal choices. Each step builds credibility and reduces surprises during diligence.

Review three to five years of statements to show true cash flow. Remove one-time items, personal expenses, and nonrecurring inflows.

Adjust owner pay to a market level so profit reflects the company’s sustainable benefit. This gives buyers a realistic earnings baseline.

Scan capital availability, buyer appetite, and industry trends that affect pricing and risk. Lenders and strategic buyers move differently in tight versus loose markets.

Track recent deals and macro signals to set timing and negotiable terms.

Use private transactions and multiples to test assumptions. Comparables validate ranges and highlight pricing surprises before marketing begins.

Count inventory and equipment, then assign value to contracts, brand equity, proprietary processes, and documented systems. Intangibles often add meaningful premium, especially in service sectors.

Translate the final figure into timing, deal structure, and preparation priorities. Decide if you should wait to improve cash flow or pursue a timely sale with protective terms.

Discipline in this process increases buyer confidence and smooths diligence, improving the odds of a clean close.

DCF models turn a multi-year forecast into a single market-ready price that buyers and lenders can discuss. The method discounts projected cash flow and then adds a terminal estimate to capture long-run worth.

A discount rate reflects the time value of money and risk. Riskier forecasts get a higher rate, which lowers present value. Keep assumptions transparent so buyers can test them quickly.

Terminal value frequently drives most implied value in a DCF, often around 75%. Small changes to growth or rate assumptions here move the total value a lot, so be conservative and evidence-based.

The exit multiple method applies a market multiple to EBITDA or EBIT in the final forecast year. It gives a market‑anchored terminal figure and is easy to explain during negotiations.

The perpetuity formula is: Terminal Value = [FCF_final_year × (1 + g)] ÷ (discount rate − g). Use realistic g and rate inputs tied to macro and sector norms.

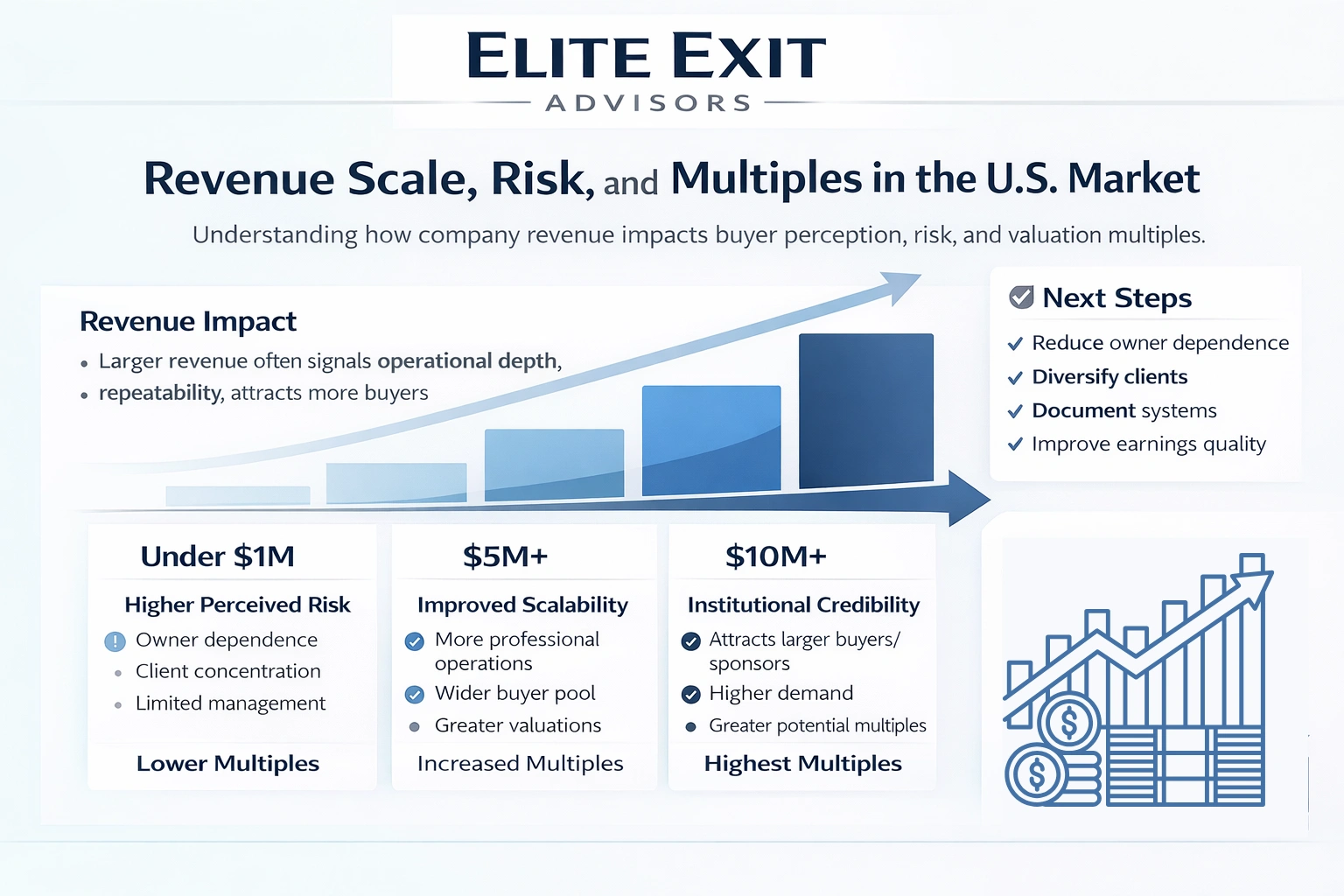

Revenue scale often shapes buyer perception more than margins do, especially across U.S. deal sizes. In the American market, headline revenue signals operational depth, repeatability, and the pool of potential buyers.

Small companies typically face higher perceived risk. Buyers see owner dependence, client concentration, and thinner management depth.

Those issues reduce multiples because buyers forecast more downside and greater integration effort.

Surpassing about $5M usually improves perceived scalability. Operations look more professional and processes often exist.

That widens the pool of buyers and can lift valuations and competitive tension.

At $10M+, companies often gain institutional credibility. Larger buyers and sponsors take interest, increasing demand and potential multiples.

Higher scale can create more growth opportunities, but buyers still test profitability, quality of earnings, and operational maturity.

What to do next: reduce owner dependence, diversify clients, document systems, and improve earnings quality to close the growth gap that suppresses multiples.

A planned five-to-ten-year timeline gives leaders time to deepen talent, diversify customers, and sharpen profits. Start with a clear benchmark and repeat the assessment every 12–18 months.

Focus on margin management, recurring contracts, and better forecasting. Remove nonrecurring items and show stable cash generation across several periods.

Differentiate with proven outcomes, steady pricing discipline, and clear proof points that justify premium multiples. Buyers look for defensible demand and repeatable growth.

Document operations, assign leads, and test transition scenarios. Demonstrated operational independence lowers buyer risk and increases confidence in closing.

Preparing early turns uncertainty into a clear plan that leaders can act on when timing shifts. Elite Exit Advisors uses valuation as a decision tool, not just a report. That approach helps owners convert a number into prioritized steps that protect value and reduce surprises.

We partner with owners and leadership teams to shore up transferable value drivers and cut owner dependence. The work centers on practical, measurable improvements that buyers actually care about.

On a call, we discuss goals, likely timing, current performance, and the data needed next. You’ll leave with clear expectations and an initial roadmap that links valuation findings to sensible steps.

Outcome: structured preparation increases confidence with buyers, reduces friction in diligence, and expands real options at closing. Book a call to turn an estimate into a plan that raises certainty and success potential.

A thoughtful exit doesn’t happen by chance; it’s built through deliberate planning, clear valuation insight, and disciplined execution over time. When you treat valuation as a strategic tool rather than a last-minute exercise, you gain clarity, control, and leverage long before a transaction begins.

Understanding what truly drives value, addressing risks early, and aligning the business with buyer expectations transforms an uncertain future into a confident, well-timed exit. Whether a sale is years away or approaching sooner than expected, a valuation-led strategy ensures you’re prepared to exit on your terms, protect what you’ve built, and realize the full worth of your business.