Business exit planning is the strategic process of preparing a company and its owner for a future transition of ownership or control, whether that’s through a sale, transfer to family or employees, merger, or other exit routes. It goes beyond just thinking about when you’ll leave; it defines how you’ll maximize value, protect your financial future, and ensure a smooth transition for all stakeholders.

Exit planning aligns your personal financial goals with your business strategy and addresses legal, tax, and operational aspects long before the actual exit occurs. Despite its importance, about 50% of business owners lack any formal exit strategy, leaving many unprepared when the time comes to move on.

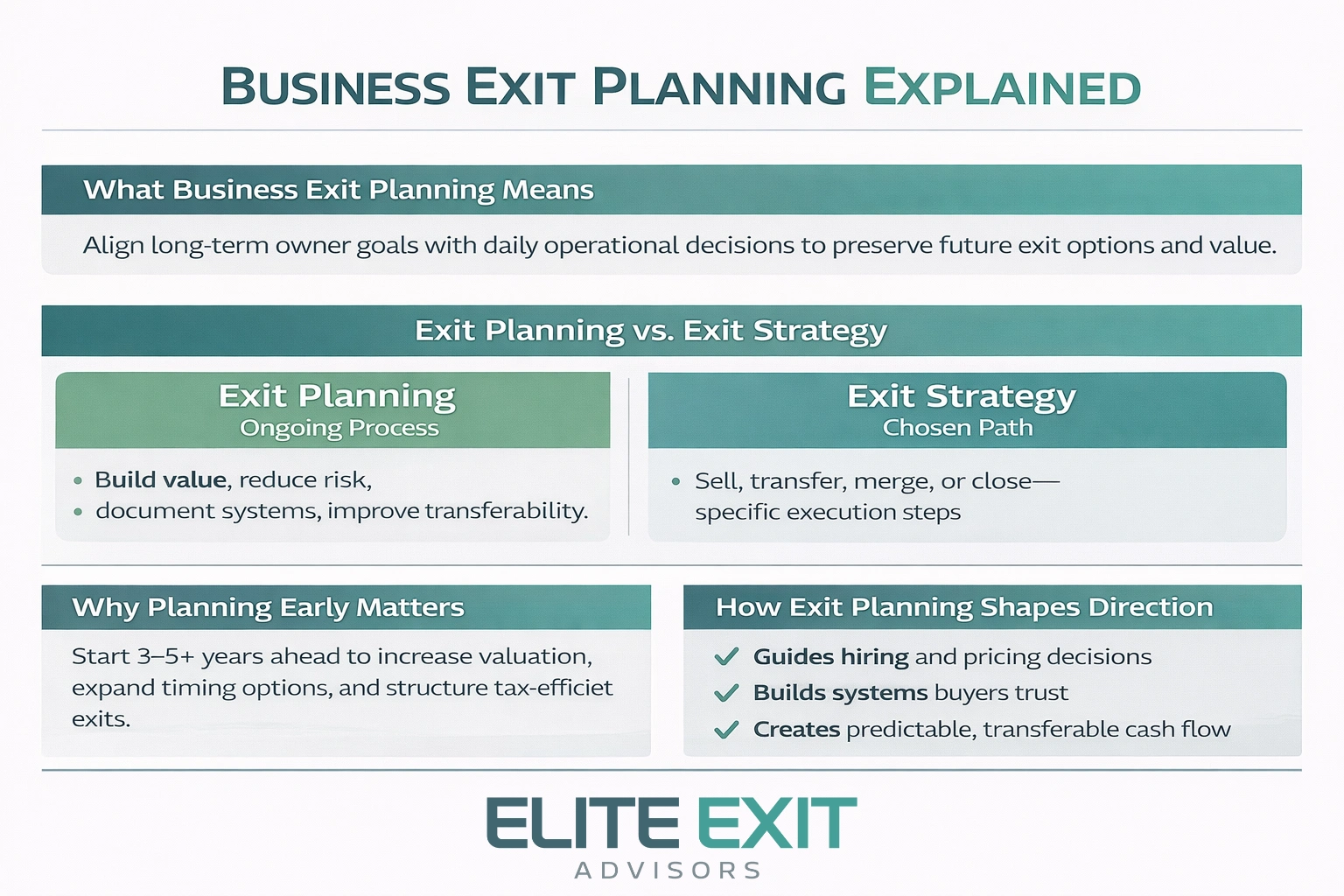

Owners today must align their long-term goals with clear operational steps to keep options open when change occurs. In the current market, that alignment turns daily choices into future value.

Exit planning is an ongoing process of improving value, reducing risk, and documenting systems. Anexit strategyis the chosen path, sell, transfer, merge, or close, with the specific steps to carry it out.

Start 3–5+ years ahead to widen timing choices, raise valuation, and explore tax-efficient structures. Early work avoids taking the first offer that appears when circumstances force a move.

A writtenexit planbecomes a management tool. It guides hiring, pricing, systems, recurring revenue, and risk controls so prospective buyers see stable performance.

Preparing for a future transfer turns uncertain events into manageable decisions today. An exit plan is not pessimistic; it is a value and risk management tool that keeps the company investable and resilient now.

Prioritizing value and profit changes daily choices. Owners who track cleaner financials, protect margins, and limit customer concentration see steady gains.

Those moves also lower operational fragility and reduce overall risk, making performance easier to prove to third parties.

“Attractive” today means repeatable growth, documented processes, and leadership depth. These features shorten due diligence and raise buyer confidence.

Heavy owner dependence creates a valuation drag. If a firm cannot operate without the owner, buyers discount price or demand longer earn-outs and tighter terms.

Link the plan to personal goals like retirement income and lifestyle. Separate personal expenses from operations before a sale to preserve proceeds and avoid surprises.

A clear timeline gives owners the room they need to shape value and protect options. Start with an intentional window rather than a fixed date. That creates breathing room to act when market conditions and personal goals align.

A multi-year runway buys time to improve financials, diversify clients, and build leadership. It also allows tax-efficient strategies that require years to implement.

Typical windows and what you can achieve in each:

Divorce, disability, death, serious illness, burnout, or key staff departures can force a rushed move. Having a plan in place protects family, employees, and customers when changes occur.

Timing affects leverage: more time means a competitive process and stronger offers. Treat this as an annual review that evolves with health, goals, and market signals so you can exit on your terms in the future.

Decide now what matters most, timing, who takes over, and how much you need, then work backward. Clear goals guide every later choice and keep emotions from driving decisions.

Pick a timing window: near-term (12 months), medium (3 years), or longer (5+ years). Each horizon allows different actions to raise value and reduce risk.

Think through internal successors (family members, key employees) and external buyer types. Internal transfers may use gifting, share transfers, or seller financing.

Match the buyer to your financial and legacy goals. Protecting staff, culture, and community often matters as much as price.

Base your target on objective valuation and net-after-tax needs, not effort or comparisons. Estimate required net proceeds after fees and tax to fund future income and goals.

Model post-transfer income needs. A common rule-of-thumb is about 75% of current income, but personal costs and business-paid expenses vary.

Document non-financial goals too: maintaining a minority role, protecting employees, or staying local. If goals exceed likely proceeds, you may need to extend the timeline, build more value, or adjust expectations.

Assembling the right advisor group early keeps complex choices coordinated and reduces costly last-minute fixes. Owners often try to manage everything alone, but legal structure, tax positioning, and documentation are hard to fix once offers arrive.

Form a core team that connects company transition decisions to personal wealth and risk management. Typical roles include an attorney, accountant, financial advisor, valuation expert, and trust and estate support.

An attorney handles letters of intent, purchase agreements, enforceable non-competes where applicable, and seller risk protection. In the U.S., they also advise on entity structure changes and regulatory matters.

The accountant cleans financials, normalizes EBITDA/SDE, and readies reports for due diligence. They also help shape a tax strategy to reduce tax drag and preserve net proceeds.

A financial advisor models post-transfer cash flow, builds investment plans, and aligns outcomes with retirement and family objectives. They close the gap between sale proceeds and long-term goals.

Beyond a number, a valuation expert explains methodology, validates market assumptions, and identifies value drivers and weaknesses to address before marketing the firm.

Trust and estate counsel coordinates ownership transfer with family goals and long-term wealth transfer. Integrated work prevents surprises for heirs and preserves tax efficiency.

A realistic business valuation for an exit strategy gives owners a fact-based picture to guide major decisions. Many owners lack recent analysis and overvalue their firm. That gap creates poor timing and weak negotiating positions.

Owners often confuse revenue with profit. Emotional attachment and “sweat equity” also inflate expectations.

Concentration risk and undocumented processes get ignored. These issues cut offers quickly when a buyer digs deeper.

A credible valuation looks beyond numbers. It reviews financial performance, customer quality, repeatable growth, defensibility, and intangibles like brand and relationships.

Contracts, IP, and leadership depth are included so the result reads as a market-ready score, not a hopeful estimate.

Use a defensible assessment as an anchor in negotiations. It adds confidence, supports competitive bidding, and can justify a premium when evidence exists.

Investors and lenders also respond better to documented value; credibility improves deal terms for growth capital or partial transfers.

Treat valuation as an action checklist. Fix owner dependence, low margins, or missing documentation first. Those fixes raise transferable value and reduce risk when buyers or investors review the opportunity.

A simple value-versus-needs check reveals whether to speed up, adjust goals, or invest in growth. Use this as a decision tool, not a prediction.

Asset gap = current company value minus retirement needs. If the result is negative, there is a shortfall to address.

Both sides must be evidence‑based: use a recent valuation and a realistic income forecast. Avoid wishful thinking when you set assumptions.

Three practical responses work well: continue operating to grow cash and value, reduce post-transfer goals and spend, or implement value-building moves now.

Internal transfers often pay over time while external sales usually deliver more cash at closing. Match the response to your timing and risk tolerance.

Small, targeted upgrades to systems and leadership often deliver the biggest return when you prepare to transfer ownership. These moves raise current profit while widening future options for a sale or transfer.

Map responsibilities and limits for key roles. Set approval thresholds and clear KPIs so others can act without constant sign-off.

Train at least two employees to manage critical functions. Cross-training prevents one-person failure and strengthens leadership depth.

Create an org chart, SOPs, pricing rules, vendor lists, and customer lifecycle maps. Record how major decisions get made and who signs off.

Well-organized operations shorten diligence and reduce perceived risk, which often improves deal terms.

Diversify lead sources, boost retention, and add recurring revenue where possible. Track metrics that prove performance, not promises.

Build contingency coverage, basic cybersecurity, and clean contract practices to protect cash flow and resilience.

Owners face two clear paths when they decide to move on: transfer the firm to a buyer or wind down operations and sell assets. Each option has trade-offs for value, timing, and risk. Choose the path that matches performance, liabilities, and personal goals.

Selling aims to convert ongoing cash flow, goodwill, and growth potential into a purchase price. Selling is realistic when financials are strong, operations run without the owner, and growth looks sustainable.

In that case, competitive offers often boost value and reduce seller risk, as they shift obligations to the buyer.

Closing monetizes assets and settles obligations rather than transferring an ongoing concern. This path makes sense when buyer interest is low, performance is in decline, or liabilities outweigh likely sale proceeds.

Liquidation can be gradual or rapid. Gradual wind-down preserves income but slows closure. Rapid liquidation speeds cash recovery but may reduce asset value and upset stakeholders. Tax timing also differs between approaches.

Both choices affect employees, customers, and other stakeholders. A sale may preserve jobs and service continuity. A closure often means layoffs, contract terminations, and customer disruption.

Clear communication reduces uncertainty and protects reputation. Plan notifications, severance or final pay, and transition support to lower disruption.

Closing checklist: file dissolution documents, cancel registrations and licenses, comply with labor laws for final pay, file final tax returns, and retain tax and financial records for 3–7 years.

Owners can choose several clear routes to transfer ownership, each with distinct trade-offs in control, timing, and proceeds. Review practical options and match one to your financial and succession goals.

Transferring to a family member preserves legacy and control but often creates conflicts. Readiness and relevant experience matter more than bloodline.

Balance “fair vs equal” when multiple family members are involved and document roles to avoid disputes.

Sales to key employees keep culture and leadership continuity. Employees often lack full capital, so phased payouts or seller financing are common.

ESOPs can provide tax benefits and broad employee ownership. They require valuations, governance changes, and stable management to work well.

Outside buyers usually bring more capital and faster liquidity. This route involves deeper diligence and possible operational change after closing.

A merger can create scale or new markets. It may also force redundancy cuts, so assess cultural and operational fit carefully.

Asset sales convert tangible items to cash but often leave goodwill unrealized. Use this way only when other transfers are infeasible.

Deal terms matter as much as price. They define who carries risk, how long the seller remains tied to results, and when capital reaches personal accounts. Choose structures that match your time horizon and tolerance for post-closing responsibility.

Installment sales and seller financing let an internal buyer purchase over time when upfront capital is limited. Payments are scheduled, often with interest, and may include a balloon at maturity.

These approaches expand the pool of buyers but increase seller credit risk if revenue falls. Use security (collateral) and clear performance covenants to reduce that risk.

Holding a minority stake for 3–7 years supports continuity and signals confidence to the buyer and team. A phased transfer can improve eventual proceeds and smooth leadership handoffs.

Compare three trade-offs:

Practical takeaway: model structures with tax and personal cash needs in mind. The headline price is one input; timing, security, and covenants shape your net outcome as much as any number on a term sheet.

Well-prepared records and clear processes make verification quick and keep negotiations on your timetable. Treat due diligence as the buyer’s verification work: it confirms claims and exposes gaps. Sellers who prepare early control time and preserve leverage in talks.

Financial essentials include clean P&Ls, reconciled balance sheets, and consistent accounting methods. Add normalized add-backs and supporting documents for major revenue items.

Show performance proof with cohort retention, pipeline/backlog quality, customer concentration analysis, and margin consistency. These items turn assertions into verifiable facts for potential buyers.

Document SOPs, list key vendor and customer contracts, and map roles so buyers see who owns day-to-day tasks. Compliance basics and organized contract folders speed review and reduce friction.

Assess risk areas: pending litigation, HR issues, cybersecurity gaps, insurance limits, and operational bottlenecks. Addressing these early often prevents price reductions or large escrow holds.

Today buyers focus on resilience without the owner, repeatable growth, and any recent changes that may disrupt revenue after closing. Deliver clear valuation support and timely reporting to back your story.

A written ownership agreement turns surprise departures into managed transitions. Legal steps protect ownership value, reduce conflict, and set clear processes for when life events force a change.

When a buy-sell agreement matters most: multiple owners, family ownership, or closely held member groups with tied finances. In those settings, an enforceable agreement prevents rushed sales and disputed control.

Core triggers to cover include divorce, disability or serious illness, death, burnout, and sudden departures of key leaders.

Without written rules, these events can force distressed sales, litigation, or leadership gaps that harm customers and vendors.

Legal planning should be part of the broader plan that includes value-building, tax work, and leadership development. Well-drafted agreements create options that advisors and owners can actually execute when change arrives.

Early tax work shapes how much of a sale you actually keep. Start years ahead to allow entity changes, timing shifts, and transfer designs that reduce liabilities. Immediate fixes rarely match the benefits of multi-year strategies.

Entity moves, like converting structure or creating a trust, often require time to take full effect. Tax rules and valuation windows can favor gradual changes over last-minute edits.

Delaying this work risks limited choices and higher taxes at closing.

Tax drag is the gap between the headline price and what the owner nets after federal and state tax, fees, and deferred payment risk. Minimizing that gap means aligning timing of proceeds with personal income needs.

Structures such as staggered payments, seller financing with security, or partial equity transfers can lower immediate liability and smooth cash flow.

Coordinate transfers with estate counsel to use trusts, charitable vehicles, or gifting where appropriate. These tools can preserve legacy goals while managing transfer tax effects.

Always align legal documents, valuation work, and advisor advice so strategies are executable when a sale or transfer happens.

A smooth leadership handoff signals maturity and raises confidence among people who depend on the firm. Visible depth in senior roles reduces perceived risk and helps preserve value during a planned or unplanned exit.

Pick candidates who match strategy and culture, not just technical ability. Look for decision-making style, credibility with employees, and rapport with key customers.

Map core functions and assign clear owners. Define KPIs and decision rights so employee roles run without constant owner input.

Follow a sequence: owners and investors first, then employees, then customers. Use empathetic, factual messages focused on continuity and next steps.

Keep policies and practices consistent while new leaders settle in. Consistency protects retention and prevents revenue disruption.

Owners gain optionality when advisors connect operational fixes, valuation insight, and tax work into a single process. That integrated approach widens choices, lowers surprise risk, and improves net outcomes over time.

Elite Exit Advisors acts as a planning-led partner for U.S. owners who want to protect value, reduce risk, and move on intentional terms rather than under pressure.

Elite Exit Advisors can help you:

Book a call with Elite Exit Advisors to start a practical, timeline-based plan tailored to your goals and options.

Small steps now unlock clearer options, better offers, and fewer surprises later.

Treat exit planning as present-tense work that improves how your firm runs today. Clarify goals, gather an advisor team, get a credible valuation, and close any asset gap before you settle on an exit strategy.

These actions raise value, reduce diligence surprises, and create a firm that can operate without constant owner involvement. The right option depends on liquidity needs, legacy priorities, timeline, and stakeholder effects.

Remember: tax outcomes, deal structures, and leadership transitions work best when started years, not weeks, ahead. Revisit the article checklists now and begin documentation, valuation conversations, and timeline planning to protect future outcomes.